Lesson 1 – Intro

This is not a “get rich quick scheme”. If you are serious about your financial well-being, and you are patient and can follow rules, then let me show you what we do. It’s all about not taking losses and growing your portfolio.

Dividends and Trading Profits

- Dividends are the number one goal of all good investors.

- Trading profits are secondary but necessary.

- The aim is to have as many occurrences as possible of both.

- Understanding the differences between unrealized and realized gains is imperative.

- Not taking losses is the key to your short-term and long-term success.

Investing vs Day Trading vs Options Trading vs Futures Trading

- Leveraging capital is a fast way to win or a fast way to lose.

- Any product that has a time limit placed on it to perform can again be positive or negative.

- The allure is the speed at which you can become rich. It also means how fast you can become poor.

- Everyone has the built-in desire of “greed”.

- There are ways to use these products, but not in the ways they are being marketed.

Even with statistics like this, there are still many that want to try and beat the odds. And this is where the market gets its bad rap as being a “casino”. I’m sure you have a friend that never loses at the casino. There are a few that do succeed in making a positive impact in their portfolio, but this comes at great sacrifice in time and resources and above all else stress. All the most successful investors can be found pretty easily online.

Emotions

When you take a loss, that triggers a negative emotion. When you make a profit, that triggers a positive emotion. We want lots of positive reinforcement so that means we need it to happen as many times as possible. We call these moments in time occurrences.

New Trader

When entering the financial markets it can be very intimidating for a newcomer. Many learn from trial and error, others dive in and spend large sums of money on Black Box systems, charting software packages, or following people like Jim Cramer on Mad Money. Lots of bells and whistles, excitement, promises of newfound fortunes. All the while legal, many folks end up losing what little they had and have to start over down possibly one of the other dead-end paths after they blow up their accounts. The main takeaway is to not follow the crowd. And this is what we call negative reinforcement.

In the workforce

Most larger companies provide some kind of 401k, profit sharing, or something along those lines. They tend to be either growth-oriented, conservatively managed, or something in between that is managed by some financial institution that has a financial incentive. And that incentive comes from “your” money. Many in the workforce are too tired or worn out to manage their own and feel it’s worth it to let someone else manage their portfolio. Fear of making a mistake with your own money teaches you what not to do, but, if you never make the mistake yourself, it’s easy to blame those who managed your portfolio, even though they make money whether you win or lose. Relying on the institutions comes at an unforeseen cost.

Semi / Retired

You always hear the fear-mongering that to retire you will need at least 2.5 million dollars to live comfortably. I’m sorry but that is just insanity. There are several folks that retire and have little more than Social Security and what they can get by on with a part-time job or help from friends. Everyone will end up somewhere in the spectrum. The point here is that if you are waiting for the Golden Goose to lay you a golden egg or you are buying lottery tickets, you have plenty of people that for whatever reason didn’t understand that to be financially independent, you need to understand that those who understand interest, earn it. Those that do not, pay it. For those that have built the nest egg, there has never been a better time to invest your money. The only thing holding you back is what holds other investors back, debt and fear.

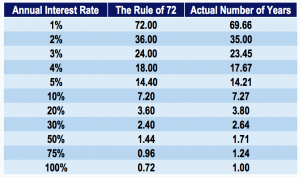

Compounding Interest

Although it’s not perfect, it is good enough for us. The dividend yield is your annual interest rate. Using the rule of 72 will give you a pretty fair idea of how long it will take you to double your money. Many though, don’t understand the differences between the dividend yield and the dividend amounts and how they interact with the price. Looking at a stock valued at $20 with a yield of 10% annual percentage yield, you would expect to make $2 for each share you have. If the price moves up, the dividend yield will move down given you are still paid the same $2 per share per year. And vice versa, the price goes down the yield will increase. And this is why it is imperative that you understand that the dividend amount is the key. The yield lets you know how hard your money is working. It does not however affect our decision based on the price, it is simply a metric that can be used to make informed decisions when used with other metrics. Too many folks want to chase the yield. Just remember all yields are not created equal yields can be misleading.

Words of wisdom

I will start by saying, and it’s not a knock on anyone, but most people are trying to solve money problems they have spent years getting themselves into with short-term answers. And this is a recipe for disaster. Debt is everywhere at different degrees and keeps you boxed in from making smart money decisions.

Debt has a compounding effect on your investing style in a negative way. You will hear of leveraged trading, margins, loan rates, etc. These will all undoubtedly put you in a bad position as we and others like to call it FOMO. We look at debt as an ongoing loss, so first things first, if you are in debt before you do anything else, get out of debt. Seek out help, maybe someone like Dave Ramsey or some other financial advisor. You can thank me later. If you are not debt-free, you can still learn and follow the system so when you do get to a point that makes sense you can benefit from what we are teaching.

There is a short quiz to complete.

Starting in the next lesson we will break down the DCT process into its various parts.